You've decided to remodel. Now comes the part most homeowners spend too little time on: figuring out how to pay for it.

Portland remodeling projects range from $25,000 for a bathroom to well over $200,000 for a whole-home renovation. Few homeowners write a check for that. Most need financing. The option you choose affects your total project cost, your timeline, and your monthly budget for years after the last trade walks off the job.

Here's an honest breakdown of every financing option available to Portland homeowners in 2026.

What You're Financing

Before comparing loan products, get a realistic number. Portland remodeling costs by project type:

| Project | Typical Range |

|---|---|

| Bathroom remodel | $25,000-$75,000 |

| Kitchen remodel | $40,000-$120,000 |

| Whole-home renovation | $100,000-$300,000+ |

| Accessory Dwelling Unit (ADU) conversion | $80,000-$180,000 |

| Deck or outdoor living | $15,000-$60,000 |

Once you have a budget range, add 15-20% for contingency. Portland's older housing stock means surprises behind walls. That contingency isn't pessimism. It's experience.

Your Financing Options

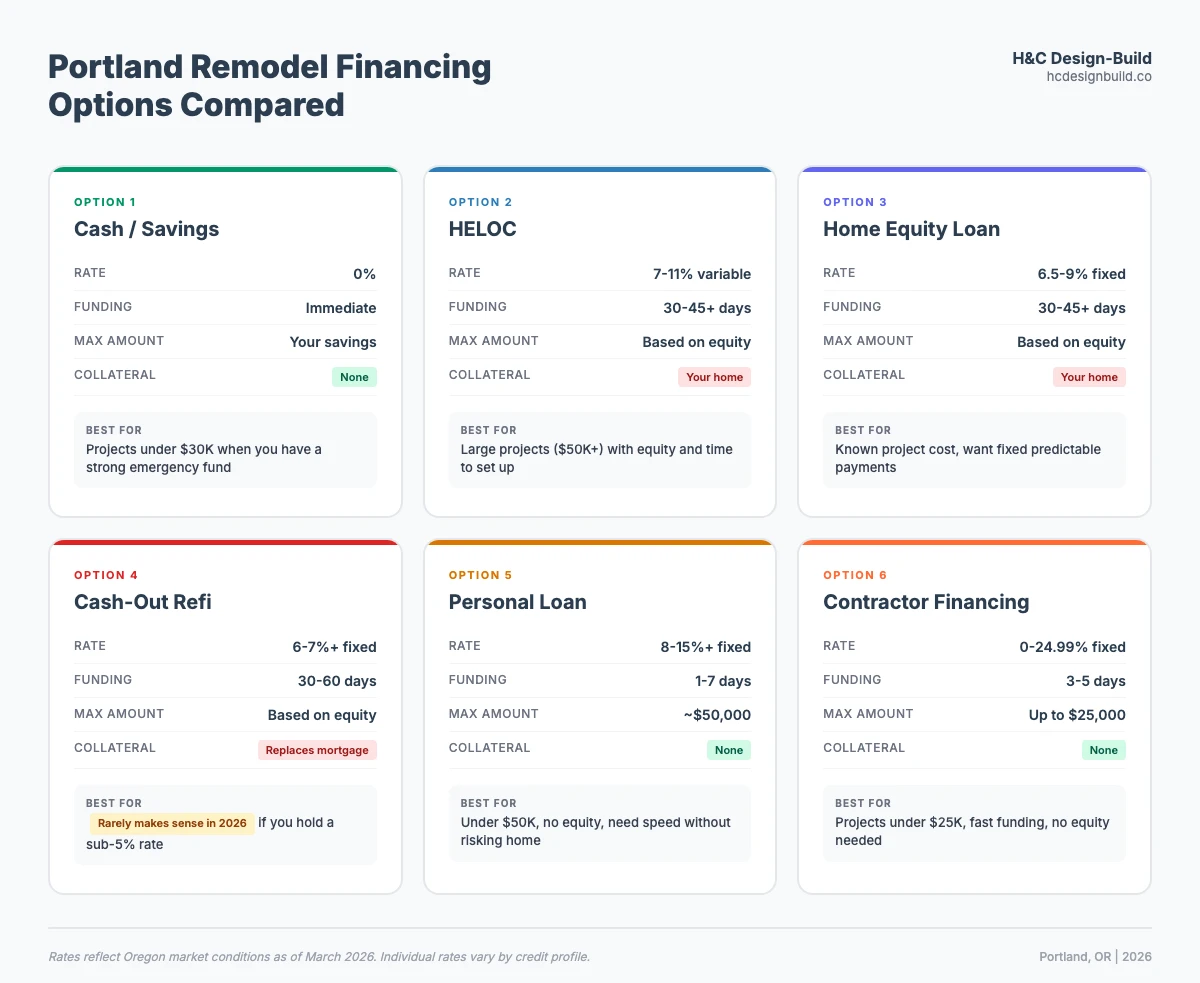

Cash or Savings

The simplest path. No interest, no monthly payments, no applications.

Cash makes sense when you can cover the full project plus contingency without draining your emergency fund. For projects under $30,000, this is often the right call.

The tradeoff: you lose liquidity. That $80,000 in a high-yield savings account earning 4-5% is working for you. Pulling it out for a kitchen remodel means losing that return. Run the math for your situation before assuming cash is automatically the best move.

HELOC (Home Equity Line of Credit)

HELOCs let you borrow against your home equity as needed, similar to a credit card secured by your house.

Current Oregon HELOC rates run 7-11% variable (opens in new tab), depending on your credit profile and lender. Oregon credit unions tend to offer the most competitive rates.

Works well when: You have significant equity, want flexible draws, and can start the process 60 days before breaking ground. Best for projects over $50,000.

Watch out for: Your home is collateral. Variable rates mean your payment can increase. Setup takes 30-45 days, sometimes longer. Closing costs run 2-5% of the credit line.

Home Equity Loan

A fixed-rate, lump-sum loan secured by your home. You get the money all at once and repay in equal monthly installments. Current Oregon rates sit around 6.5-9% fixed.

Works well when: You know your exact project cost and want payment predictability. The fixed rate removes the variable-rate risk of a HELOC.

Watch out for: Same equity and collateral requirements as a HELOC. Same slow timeline. You borrow a fixed amount, so estimate carefully.

Cash-Out Refinance

Replace your current mortgage with a larger one and pocket the difference.

In 2026, this rarely makes sense. Over half of Portland homeowners (opens in new tab) hold mortgage rates below 4%. Refinancing to today's roughly 6% rates (opens in new tab) means paying more on your entire mortgage balance, not just the cash-out amount.

On a $400,000 mortgage, resetting from 3.5% to 6.1% costs an extra $630 per month. We covered this math in our remodel vs. move analysis.

Cash-out refinancing only makes sense if your current rate is already at or above today's rates. For most Portland homeowners, it's the most expensive option on this list.

Personal Loan (Unsecured)

A fixed-rate loan that doesn't use your home as collateral.

Works well when: Your project is under $50,000, you lack home equity, or you want to keep your home off the table. Approval and funding often happen within days.

Watch out for: Higher rates (8-15%+ depending on credit), shorter terms (2-7 years) that mean higher monthly payments, and interest is not tax-deductible.

Contractor Financing (U.S. Bank Avvance)

H&C Design-Build partners with U.S. Bank Avvance to offer project financing directly through your contractor.

How it works:

- Pre-qualify with a soft credit check. No impact to your credit score.

- See your approved amount and available terms.

- Choose a loan that fits your monthly budget.

- H&C receives funding within 48 hours of finalization.

Key details:

- Loan amounts up to $25,000

- Fixed terms from 3 to 60 months

- APR from 0% to 24.99%, depending on creditworthiness

- Based on credit profile, not home equity

- Your home is not used as collateral

Where this fits: Projects under $25,000 like bathroom refreshes, deck builds, window replacements, and accessibility modifications. Also useful as supplemental financing alongside savings or a HELOC to cover overages.

The main advantage is speed. Pre-qualification takes minutes. Full funding completes in days, compared to 30-45+ days for equity-based products. If your contractor has availability now, waiting six weeks for a HELOC can push your project to the next season.

Our financing page has full details and a pre-qualification link. Using it is optional. You're welcome to use any financing method.

Comparison at a Glance

| Option | Rate Range | Funding Speed | Typical Max | Home as Collateral? |

|---|---|---|---|---|

| Cash | 0% | Immediate | Your savings | No |

| HELOC | 7-11% variable | 30-45+ days | Based on equity | Yes |

| Home equity loan | 6.5-9% fixed | 30-45+ days | Based on equity | Yes |

| Cash-out refi | 6-7%+ fixed | 30-60 days | Based on equity | Yes (replaces mortgage) |

| Personal loan | 8-15%+ fixed | 1-7 days | ~$50,000 | No |

| Contractor financing | 0-24.99% fixed | 3-5 days | $25,000 | No |

Which Option Fits Your Situation

You have equity and time. HELOC or home equity loan. Start the application 60 days before you plan to break ground.

You need to move fast. Contractor financing or a personal loan. If your contractor has availability now, waiting 45 days for a HELOC can cost you more than the rate difference when material prices are climbing.

You want your home off the table. Contractor financing, personal loan, or cash. No foreclosure risk if something goes sideways.

You hold a low mortgage rate (under 5%). Avoid cash-out refinancing. Any other option costs less over time.

Your project is under $25,000. Cash, contractor financing, or a personal loan. The closing costs on equity products eat into the benefit at smaller loan amounts.

Your project exceeds $100,000. HELOC or home equity loan is the practical path. You can supplement with contractor financing or savings if your equity line falls short.

Oregon-Specific Considerations

Property Tax Impact

Oregon's Measure 50 (opens in new tab) normally caps assessed value growth at 3% per year. Remodeling is an exception. Significant improvements can trigger a reassessment beyond the cap.

The increase is based on the value the improvement adds, not the full market value of your home. A $60,000 kitchen remodel won't double your tax bill. But factor the increase into your long-term budget.

Energy Rebates Reduce What You Finance

Portland homeowners can offset remodeling costs with energy rebates before financing the balance. Energy Trust of Oregon incentives (opens in new tab), Portland Clean Energy Community Fund (PCEF) grants, and upcoming Oregon HOMES/HEAR rebates (opens in new tab) can cover $5,000-$15,000+ for qualifying improvements.

If your remodel includes heat pump installation, insulation, windows, or electrical panel upgrades, apply for rebates first. Finance the remaining balance. Our energy rebates guide covers every available program.

Federal Tax Credits

The IRS Section 25C energy efficient home improvement credit (opens in new tab) expired December 31, 2025. If you installed qualifying improvements (heat pumps, insulation, windows, exterior doors) before that date, you can still claim the credit on your 2025 tax return. For 2026 installations, the credit is no longer available unless Congress passes new legislation.

Accessibility modifications prescribed by a doctor may still qualify as a medical expense deduction. If your remodel includes aging-in-place features like curbless showers or wider doorways, ask your tax advisor about eligibility.

Budget Rules That Work

The 80% rule. Finance 80% of the maximum you can comfortably afford. Keep 20% as a buffer for scope changes, hidden conditions, or material swings. Portland's pre-war homes regularly reveal surprises during demolition.

Match the loan term to your stay. Planning to sell in five years? A shorter-term loan with higher payments makes more financial sense than stretching payments over 15 years of interest.

Don't finance beyond the value added. If a $60,000 kitchen remodel adds $50,000 in home value, you're carrying $10,000 in debt with no backing asset. That's fine if you're remodeling for livability. Just go in knowing the math.

Red Flags in Contractor Financing

Not all contractor financing is transparent. Watch for:

- Deferred interest ("Same as cash"). If you don't pay in full by the promotional period end, you owe interest on the entire original balance. These deals look good and get expensive fast.

- Balloon payments. Low monthly payments with a large lump sum due at the end. Understand the full payment schedule before signing.

- Mandatory financing. A contractor who requires you to use their financing partner may be earning a referral fee that inflates your project cost.

- No written terms before signing. You should see the APR, total interest cost, and full payment schedule before committing to anything.

H&C's partnership with U.S. Bank Avvance is optional. We offer it as a convenience, not a requirement.

This guide is for informational purposes only and does not constitute financial, tax, or legal advice. Consult a qualified financial advisor or tax professional before making financing decisions.

The right financing choice depends on your equity position, timeline, risk tolerance, and project size. Run the numbers, compare two or three options, and factor in how long you plan to stay in your home.

If you're planning a Portland remodel and want to understand both the project cost and financing options, reach out. We'll walk through the numbers with you.

Frequently Asked Questions

What is the cheapest way to finance a home remodel in Portland?

Cash costs nothing in interest. For borrowing, HELOCs offer the lowest rates in Oregon (currently 7-11% variable) but require home equity and take 30-45 days to set up.

Can I finance a remodel without home equity?

Yes. Contractor financing through programs like U.S. Bank Avvance, personal loans, and savings all work without home equity. Avvance loans go up to $25,000 based on creditworthiness alone.

Does remodeling increase Oregon property taxes?

It can. Oregon Measure 50 caps assessed value growth at 3% per year, but significant remodeling is an exception that can trigger a larger reassessment based on the value added.

Should I use a HELOC or contractor financing for a remodel?

HELOCs offer lower rates but take 30-45 days and use your home as collateral. Contractor financing funds in days with no equity requirement but typically carries higher rates. HELOCs suit large projects. Contractor financing suits projects under $25,000 or supplemental funding.

How much contingency should I budget for a Portland remodel?

Budget 15-20% above your project estimate for contingency. Portland's older housing stock frequently reveals hidden conditions during demolition that add cost.